Introduction

The global financial crisis of 2007 and 2008 revealed a critical vulnerability in the banking sector: many institutions lacked the technology and data architecture required to manage risks across their entire organization. In response, the Basel Committee on Banking Supervision developed Standard Number 239, which is formally titled Principles for effective risk data aggregation and risk reporting. These guidelines are designed to enhance risk management and decision-making processes by ensuring that leadership has access to accurate, timely, and comprehensive risk information.

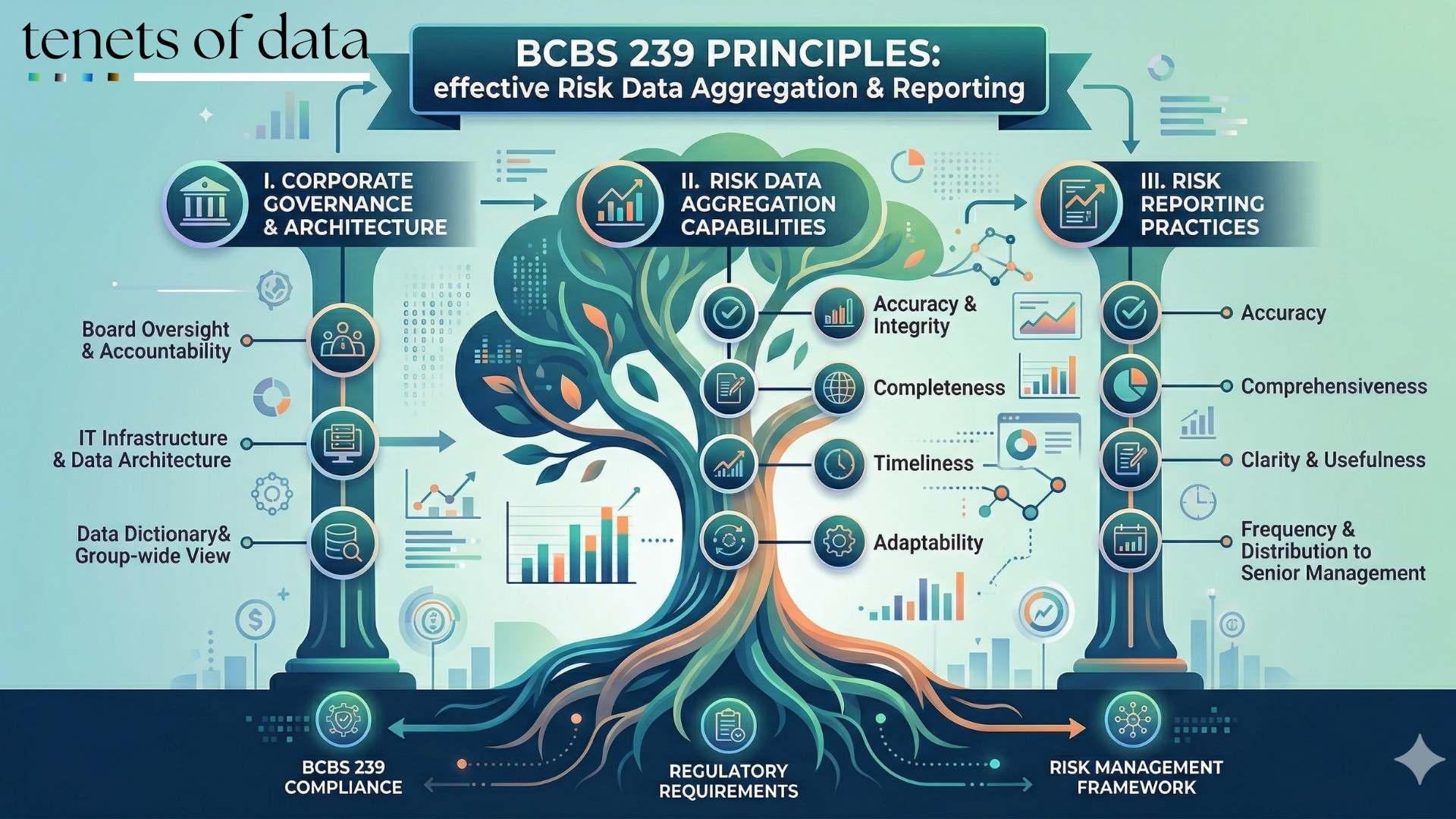

Understanding the 14 Principles

The framework defines specific expectations for how data should be managed and reported, particularly during periods of market stress.

I. Governance and Infrastructure

- Principle 1 (Governance): A bank must have strong governance arrangements where the board and senior management take ownership of risk data quality and reporting processes.

- Principle 2 (Data Architecture and IT Infrastructure): Institutions should design and maintain systems that fully support risk aggregation capabilities in both normal times and during severe crises.

II. Risk Data Aggregation Capabilities

- Principle 3 (Accuracy and Integrity): Data must be accurate and reliable, with aggregation processes being largely automated to minimize human error.

- Principle 4 (Completeness): The system must capture all material risk data across the banking group, including off-balance sheet exposures.

- Principle 5 (Timeliness): Banks must generate up-to-date risk data rapidly, with the speed reflecting the volatility and criticality of the specific risk being measured.

- Principle 6 (Adaptability): Systems must be flexible enough to meet ad hoc reporting requests during crises or in response to changing regulatory requirements.

III. Risk Reporting Practices

- Principle 7 (Accuracy): Risk reports must precisely convey aggregated data and be subject to regular reconciliation and validation.

- Principle 8 (Comprehensiveness): Reports should cover all material risk areas, with a depth and scope consistent with the bank's size and complexity.

- Principle 9 (Clarity and Usefulness): Information must be clear and tailored to the needs of the recipients, balancing technical data with qualitative interpretation.

- Principle 10 (Frequency): The frequency of report production and distribution should reflect the nature of the risks and be increased during times of stress.

- Principle 11 (Distribution): Reports must reach relevant stakeholders securely and promptly while maintaining confidentiality.

IV. Supervisory Review and Cooperation

- Principle 12 (Review): Regulators must periodically evaluate a bank's compliance with the previous 11 principles.

- Principle 13 (Remedial Actions): Supervisors must use appropriate tools to require timely remedial action if deficiencies are identified.

- Principle 14 (Home/Host Cooperation): Authorities in different jurisdictions should cooperate to ensure consistent supervision of cross-border banking groups.

Categorization of BCBS 239 Principles

The 14 principles are organized into four distinct functional categories, covering everything from internal leadership to external supervisory cooperation. The following table summarizes these pillars and their primary objectives.

| Category | Principles Included | Core Objective |

|---|---|---|

| Governance and Infrastructure | Principles 1 and 2 | Establishing senior management accountability and building resilient IT systems. |

| Risk Data Aggregation Capabilities | Principles 3 to 6 | Developing the ability to gather and process risk data accurately across the group. |

| Risk Reporting Practices | Principles 7 to 11 | Ensuring risk reports are clear, precise, and useful to senior decision-makers. |

| Supervisory Review and Cooperation | Principles 12 to 14 | Facilitating regular regulatory audits and cross-border cooperation between authorities. |

Detailed Breakdown of the Principles

1. Overarching Governance and Infrastructure

The first category demands that risk management starts at the board level. Principle 1 states that risk data aggregation and reporting must be subject to strong governance arrangements consistent with other Basel Committee guidance. The board of directors is responsible for approving the risk reporting framework and ensuring that adequate financial and human resources are allocated to maintain it. Principle 2 requires banks to maintain data architecture and IT infrastructure that fully support risk aggregation under both normal conditions and periods of severe market stress.

2. Risk Data Aggregation Capabilities

This category focuses on the technical ability to synthesize data. Principle 3 requires data accuracy and integrity, emphasizing that aggregation should be largely automated to minimize human error. Principle 4 mandates completeness, requiring institutions to capture all material risks across legal entities and geographic regions, including off-balance-sheet exposures. Under Principle 5, data must be timely, with the speed of aggregation reflecting the volatility of the specific risk being measured. Principle 6 addresses adaptability, ensuring systems can meet ad hoc requests during crises or changes in the regulatory landscape.

3. Risk Reporting Practices

The quality of the final output is governed by Principles 7 through 11. Reports must be accurate and precise to allow leadership to make confident decisions (Principle 7). They must also be comprehensive, covering all material risk areas, such as credit, market, and liquidity risks (Principle 8). Principle 9 requires clarity and usefulness, which involves balancing technical data with qualitative explanations tailored to the recipient. Principles 10 and 11 cover frequency and distribution, ensuring reports are produced regularly (especially during stress) and delivered securely to the correct stakeholders.

4. Supervisory Review, Tools, and Cooperation

Regulators play an active role in enforcement. Principle 12 empowers supervisors to periodically evaluate a bank's compliance with the previous 11 principles. If deficiencies are found, Principle 13 allows supervisors to take remedial actions, which can include capital add-ons or specific remediation plans. Finally, Principle 14 requires supervisors in different jurisdictions to cooperate and share information regarding the risk profiles of cross-border banking groups.

Working Towards Compliance: A Strategic Roadmap

Compliance with BCBS 239 is not a one-time project but an ongoing operational practice. Many institutions still struggle with implementation, with common hurdles including legacy IT systems, manual workflows, and unclear data ownership. To address these challenges, organizations can follow a structured implementation path.

- Conduct a Thorough Gap Analysis: The first step is to evaluate existing governance and technical capabilities against the 14 principles. This diagnosis helps prioritize remediation tasks based on regulatory urgency and business impact.

- Establish Data Ownership and Stewardship: Banks must define who owns specific datasets and who is responsible for data quality. Creating data governance committees and assigning RACI-aligned roles helps clarify accountability across distributed teams.

- Modernize Data Architecture and Taxonomy: Integrating fragmented legacy platforms into a centralized architecture is essential. Organizations should establish standardized data definitions (a data dictionary) for critical data elements like exposures and asset classes to ensure consistency.

- Implement Robust Data Lineage: Regulators now expect banks to demonstrate a comprehensive understanding of data flows from origination to final reporting. Implementing attribute-level technical lineage allows banks to trace how data is transformed, which is vital for validation and audit readiness.

- Automate Reporting Pipelines: Eliminating manual, spreadsheet-based reporting reduces the risk of human error and improves timeliness. Automated pipelines that extract, transform, and load risk data enable daily or even intraday reporting during volatile periods.

- Strengthen Independent Validation: The second and third lines of defense should perform regular, independent assessments of risk data aggregation and reporting capabilities. This ensures that processes are functioning as intended and remain appropriate for the bank's evolving risk profile.

- through the final report, at the attribute level, Test for Stress Scenarios: It is critical to verify that risk systems can handle sudden spikes in data volume or urgent ad hoc requests during a crisis. Simulated stress tests ensure that recovery plans and communication channels are resilient.

Strategic Roadmap Toward Compliance

Compliance is an ongoing operational practice rather than a one-time project, and many institutions still face hurdles like legacy systems and manual workflows. Organizations can follow these practical steps to align with the standard.

- **Execute a Thorough Gap Analysis:** Evaluate existing governance frameworks and technical capabilities against the 14 principles to prioritize remediation tasks by

- Formalize Data Ownership and Stewardship: Define clear roles for data owners and stewards using accountability matrices to eliminate ambiguity regarding data quality.

- Implement Technical Data Lineage: Establish end-to-end traceability of risk data from origination through the final report, at the attribute level, to ensure transparency and audit readiness.

- Modernize with Automated Pipelines: Replace manual, spreadsheet-based reporting with automated data hubs or warehouses to improve timeliness and reduce processing errors.

- Establish an Independent Validation Function: The second line of defense should perform regular, independent assessments of risk data aggregation and reporting capabilities to ensure they remain appropriate for the bank's risk profile.

- Test for Stress Scenarios: Verify that systems can handle sudden spikes in data volume or urgent ad hoc requests by running simulations of market crashes or liquidity crunches.

Conclusion

By moving beyond simple checkbox compliance, organizations can transform these principles into a strategic advantage, enabling faster insights and more resilient decision-making.

By moving beyond simple checkbox compliance, organizations can transform these principles into a strategic advantage. High-quality, well-governed data not only satisfies regulators but also enables faster insights, more resilient decision making, and the ability to leverage advanced technologies like artificial intelligence.